Filling of Appeal

Comprehensive Annual Compliance & Reconciliation

Official CMA Audit Support

Service Overview

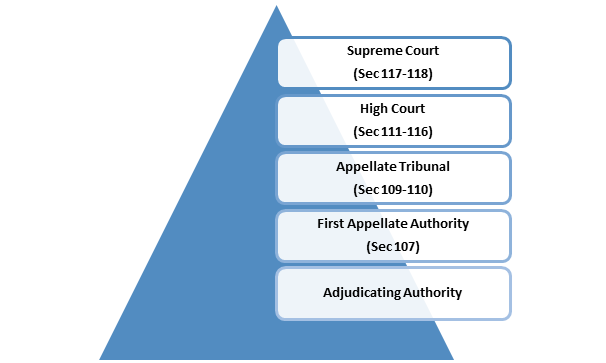

• An appeal is a mechanism by which the law provides the right to the assessee to file a complaint against the injustice done by the lower authority to the upper authority. The party complaining is called “Appellant” and the other party is known as “Respondent” • Appeals and revision are an integral part of tax laws. These provisions of appeals and revisions are provided in a legislature to protect the principles of the natural justice and provide a relief to the aggrieved by tax laws. The facts and circumstances of a particular case and the question of law involved are relevant for taking a call on jurisdiction of the appeals and revision- Appeal, Review & Revision. • The Appeal Mechanism under GST is as under • Tax laws (or any laws, for that matter) impose obligations. Such obligations are broadly of two kinds: tax-related and procedure-related. The taxpayer’s compliance with these obligations is verified by the tax officer by various instruments such as scrutiny, audit, anti-evasion, etc., as a result of which sometimes there are situations of actual or perceived non-compliance. If the difference in views persists, it results into a dispute, which is then required to be resolved. • Tax law recognizes that on any given set of facts and laws, there can be different opinions or viewpoints. Hence, it is likely that the taxpayer may not agree with the “adjudication order” so passed by the tax officer. It is equally possible that the Department may itself not be in agreement with the adjudication order in some cases. It is for this reason that the statute provides further channels of appeal, to both sides. However, since the right to appeal is a statutory right, the statute also places restraints on the exercise of that right. The time limits prescribed by the statute for filing of appeals and the requirement of pre-deposit of a certain sum before the appeal can be heard by the competent authority are examples of such fetters on the statutory right. • Section 107 provides that appeal shall be preferred before such Appellate Authority as may be prescribed. Rule 109A provides that for the purpose of appeal, an Appellate Authority shall be: • (a) the Commissioner (Appeals) where such decision or order is passed by the Additional or Joint Commissioner; • (b) the Additional Commissioner (Appeals) where such decision or order is passed by the Deputy or Assistant Commissioner or Superintendent.

Documents Required for Filing

| Sr. No. | Necessary Document |

|---|---|

| No documents required | |