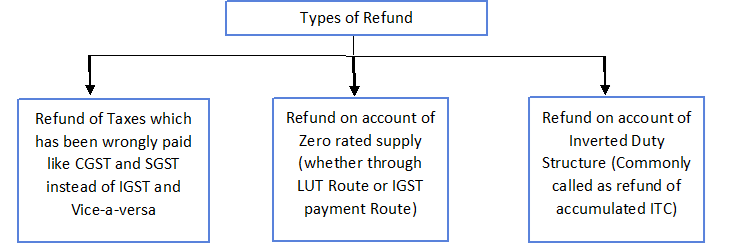

Claims for Refunds

Comprehensive Annual Compliance & Reconciliation

Official CMA Audit Support

Service Overview

● FORM GST RFD-01: Application for refund of excess ITC or tax paid. ● Statement-1: Refund claim based on GSTR-1 as amended by GSTR-1A (Rule 89(2)(a)). ● Statement-2: Refund for export of services with payment of tax (Rule 89(2)(c)). ● Statement-3: Refund for export without payment of tax (accumulated ITC) (Rule 89(2)(b) and (c)). ● Rule 89(4): Formula for refund claim for supplies to SEZ units/developers without payment of tax. ● Rule 89(11): “Adjusted total turnover” excludes exempt supplies (other than zero-rated). ● Rule 89(10): “Net input tax credit” includes ITC on inputs and input services. ● Mandatory documents: BRC/FIRC for export of services; Shipping Bill/EGM for export of goods (Rule 89(11)). ● Amendments: Refund is recalculated based on amended invoice values (Rule 89(12)). ● FORM GST RFD-01A: Used for refund claims arising from reverse charge or imports. ● Key provision: In case of reverse charge or imports, the GSTIN of the recipient (applicant) is treated as the GSTIN of the supplier (Rule 89(2)(c)).

Documents Required for Filing

| Sr. No. | Necessary Document |

|---|---|

| No documents required | |